At the opening research workshop of the ARTEMIS Final Conference, eight new studies challenged conventional wisdom on how private capital can – and cannot- be mobilised for nature and climate.

The first day of the ARTEMIS Final Conference opened not with grand declarations, but with rigorous debate. Organised by Plan Bleu (UNEP/MAP), the workshop Blended Finance for a Greener Future — Aligning Private Investment with Sustainability Goals in the Mediterranean convened researchers from across the region to confront one of the most pressing questions in Mediterranean sustainability: how do you make private capital work for biodiversity, climate adaptation and ecosystem restoration?

Led by Plan Bleu’s Constantin Tsakas, the session centred on the first presentations of eight draft research papers, a body of work that, taken together, offers both a sobering diagnosis and a forward-looking prescription for the region’s green finance architecture.

“Restoring nature at scale requires not only science and governance, but also innovative financial mechanisms capable of unlocking long-term investment.”

The core challenge

Volume is not enough

A recurring theme across the papers was a fundamental challenge to the assumption that more blended finance automatically means more climate progress. Research by Nancy Barakat Rodulf and Myriam Ramzy, studying 11 Mediterranean nations, found a troubling “suppressor” effect: when private energy investments are accounted for, blended finance flows actually correlate with higher CO₂ emissions — pointing to a fossil-fuel lock-in risk where capital funds broader capacity expansion rather than genuine decarbonisation. Their conclusion was clear: the composition and targeted quality of finance matter far more than aggregate volume alone.

Complementing this, Stella Tsani and Chrysoula Chitou introduced a new “Blended Finance Readiness Matrix” that upended the traditional North-South institutional divide. Morocco, they found, outperforms Greece in blended finance readiness — driven by superior fiscal stability and financial market depth — despite Greece’s stronger ESG alignment. But even the highest-readiness countries like Spain and Italy face a structural wall: private capital simply will not flow to ecosystem restoration projects that generate diffuse public benefits rather than monetisable cash flows.

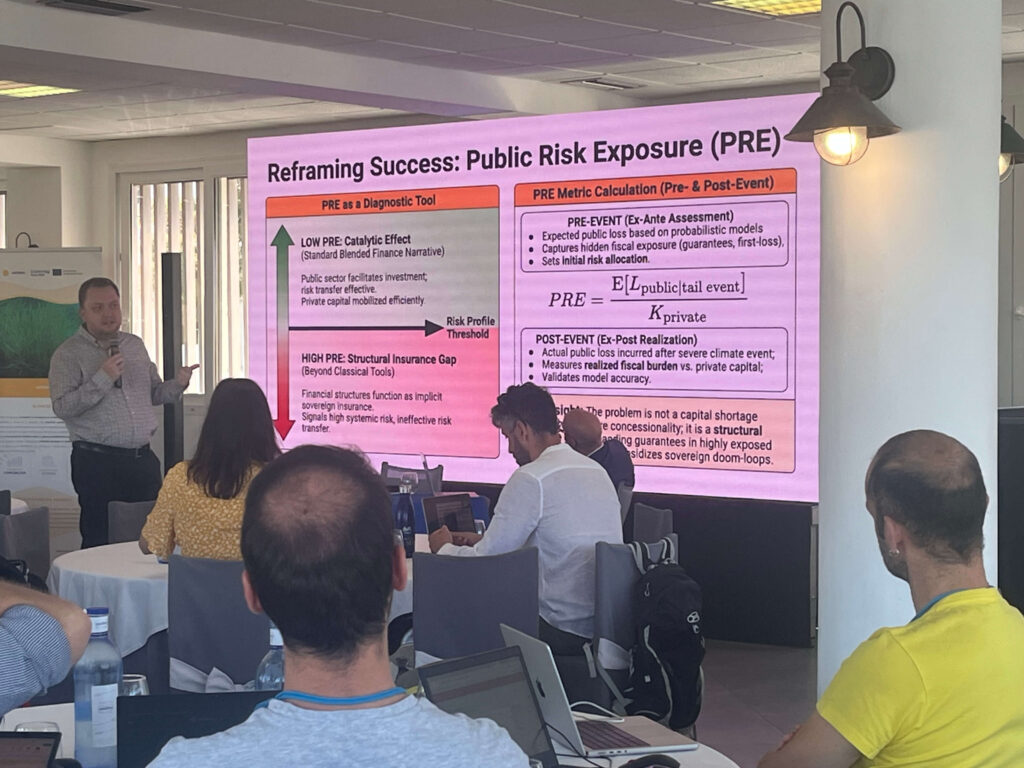

When de-risking creates hidden debt

If the financing readiness papers challenged quantity assumptions, Mehmet Murat Çobanoğlu’s contribution challenged quality assumptions in the de-risking toolkit. His paper introduced the “Public Risk Exposure” metric to demonstrate that applying conventional guarantees to adaptation risks — coastal protection, drought resilience — does not actually transfer risk to the private sector. Because adaptation risks are systemic and spatially correlated (entire regions face disasters simultaneously), standard guarantees simply create hidden sovereign debt that can explode onto public balance sheets when a shock hits. The recommended alternative: parametric insurance, catastrophe bonds, and Mediterranean-wide regional risk-pooling mechanisms.

“Applying standard corporate due diligence to smallholder farmers or waste pickers is impractical — and effectively excludes the most climate-vulnerable groups from accessing finance.”

Who gets left out

Two papers brought a sharply human lens to the discussion. Ceyhun Elgin’s work on the “formality trap” showed how blended finance instruments — built around audited financial statements, collateral and formal ESG documentation — structurally exclude informal economies. Morocco, Tunisia, Egypt and Türkiye all fall into a high-exclusion category, effectively locking out smallholder farmers, waste pickers and other climate-vulnerable actors from the very instruments designed to help them.

Dorsaf Ben Taleb Sfar’s case study of Enda Tamweel in Tunisia added a gendered dimension: standard microfinance repayment schedules are misaligned with the seasonal income patterns of women-led agricultural projects, while collateral requirements exclude women who lack formal land ownership. Her paper proposed a progressive roadmap — beginning with simple gender indicators and moving toward redesigned public guarantees that absorb the liquidity risks specific to women’s agricultural cycles.

The ocean funding gap — and a blockchain answer

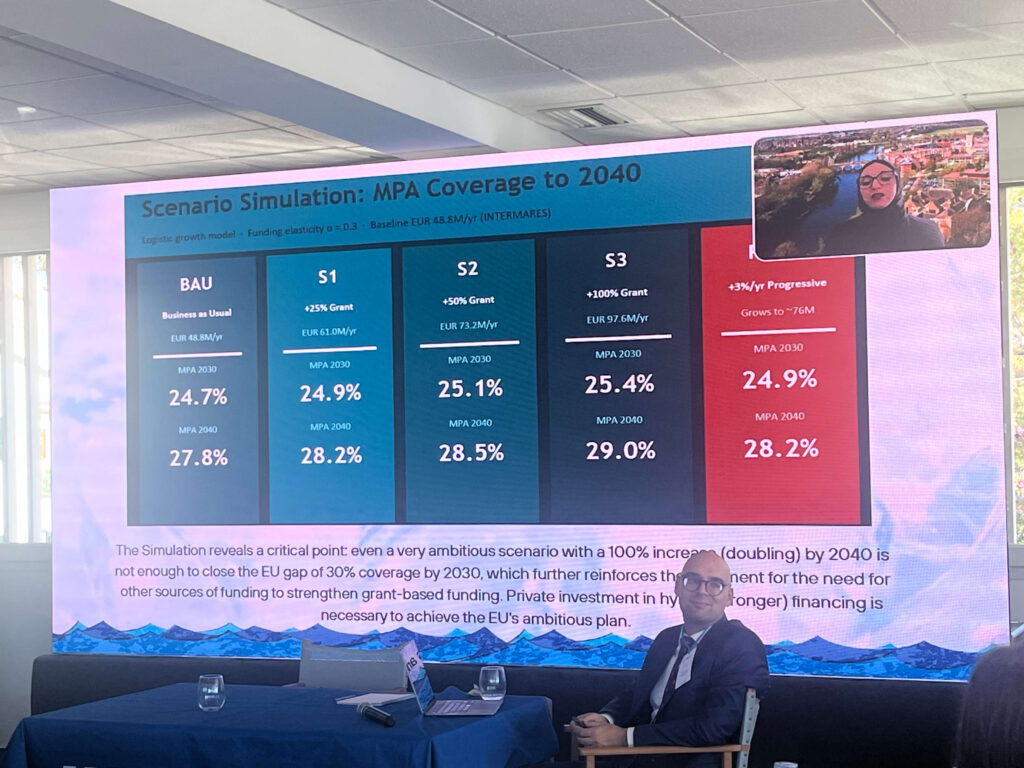

The final cluster of papers turned to the Mediterranean’s marine environment. Widad Metadjer and Zahra Derriche’s analysis of Spain’s LIFE IP INTERMARES project offered a striking projection: even doubling grant funding for seagrass restoration would still leave marine protected area coverage at only around 29% of EU targets by 2040. Their solution — converting verified ecological improvements into tradable blue carbon credits to catalyse private co-investment — opened one of the workshop’s most animated discussions.

That discussion found a natural partner in the final paper, by Fethallah Benmokhtar, Hadjer Boulila and Soumia Ykhlef, which proposed embedding blockchain-enabled governance directly into blended Blue Bonds to eliminate “blue-washing” and reduce monitoring costs. A simulation based on the ARTEMIS Posidonia project suggested that blockchain-based monitoring could reduce investor risk premiums by around 25 basis points — equivalent to approximately €1.5 million in savings on a €60 million bond over ten years.